470

We are journalists who recently published an investigation of Warren Buffett’s mobile-home empire. AUA!

Hello Reddit! We are investigative reporters: Mike Baker at The Seattle Times and Daniel Wagner at The Center for Public Integrity.

We just published an investigation about America's second-richest man, Warren Buffett, and the mobile home empire he's built over the past 12 years. While Buffett has a reputation as a responsible businessman and grandfatherly figure, we found that his company relies on predatory sales practices, exorbitant fees, and interest rates that can exceed 15 percent, trapping many buyers in loans they can’t afford and in homes that are almost impossible to sell or refinance.

We’ve been inundated with reader responses to the investigation, so we thought we’d open it up to Reddit and answer any questions people may have. Ask Us Anything.

(Here are links to the original stories: Seattle Times version / Center for Public Integrity version.)

UPDATE (3:30 pm Eastern): Thanks everyone for all the great questions! We’re signing off for now but will check back later today if there are any fresh questions. If you want to contact us directly, our emails are mbaker (at) seattletimes (dot) com and dwagner (at) publicintegrity (dot) org.

MobileHomeTrap11 karma

Regarding the first part of your question, credit risk always is a part of how loans are priced. However, Clayton’s loans are unusually costly, as Mike explained in this answer, in part because Berkshire Hathaway charges Clayton up to an extra percentage point on top of BRK’s own borrowing costs -- and that’s passed directly to the consumer. So credit risk is only one element of how the rates are set.

On your second question: Many borrowers said they were induced by Clayton sales reps to spend money preparing land or paying deposits before they found out the loan terms. These people don’t have much to spare, so they can feel trapped by the money they already have invested. -DW

stockbroker31 karma

However, Clayton’s loans are unusually costly, as Mike explained in this answer[1] , in part because Berkshire Hathaway charges Clayton up to an extra percentage point on top of BRK’s own borrowing costs -- and that’s passed directly to the consumer. So credit risk is only one element of how the rates are set.

So, you're telling me that other manufactured home lenders are paying less for their financing than Clayton?

BRK (one of the most creditworthy institutions in the world) guarantees Clayton's debt. The 1% bump probably puts it on level ground with the borrowing costs of other manufactured home lenders. Not sure why you'd expect BRK to lend to Clayton at below-market rates.

MobileHomeTrap-11 karma

You’re correct that BRK’s low borrowing costs (a result of its high credit rating) is the main reason why Clayton approached it in 2003, after demand for Clayton’s MH-backed ABS evaporated.

But Clayton is not a separate company borrowing from BRK; it is a wholly owned subsidiary whose profits all flow back to the parent corporation. And while there’s nothing inherently wrong with charging a subsidiary extra bps on top of your cost of funds, that “guarantee fee” does increase the prices charged to consumers. -DW

BunchOAtoms18 karma

Regarding the first part of your question, credit risk always is a part of how loans are priced. However, Clayton’s loans are unusually costly, as Mike explained in this answer[1] , in part because Berkshire Hathaway charges Clayton up to an extra percentage point on top of BRK’s own borrowing costs -- and that’s passed directly to the consumer. So credit risk is only one element of how the rates are set.

Nice way to avoid the question. Interest rates (particularly for individuals) are determined by factors other than their credit score, but you didn't answer the question.

Wouldn't high interest rates make sense when dealing with a demographic who are more likely to default on their payments than those who make a higher income?

So what's the answer?

MobileHomeTrap9 karma

For sure, higher interest rates do make sense for risky borrowers. Clayton, however, has particularly high rates in the mobile-home world. And some borrowers felt trapped in loans with high rates because of promises they said were made to them by dealers. --MB (comment edited to add "--MB")

The_Rusty_Taco40 karma

How do their rates compact to other subprime lenders? Is the issue strictly with Buffet's company, or the general practice of subprime lending in the mobile home market. Are most mobile home buyers considered subprime customers?

MobileHomeTrap12 karma

As a whole, mobile homes are financed at higher rates than conventional homes for a couple of reasons: First, because many of them are personal property loans like you’d get on a car, as opposed to mortgages. Second, because conventional loans benefit from various forms of government support.

It’s important to keep in mind, though, that the subprime lending business on homes has essentially been defunct since the 2008 crash. -DW

MobileHomeTrap11 karma

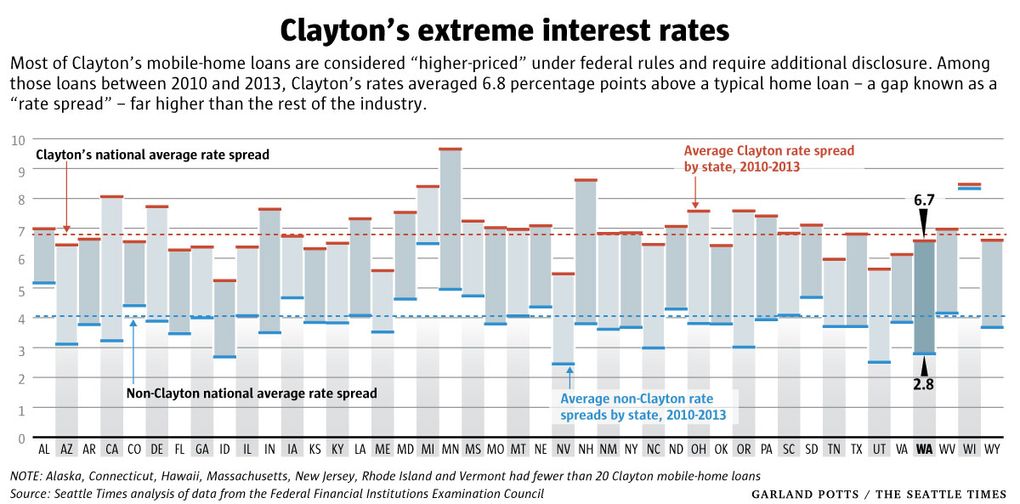

If you just look at mobile-home lenders, Clayton has some particularly costly rates. During the most recent four-year period, 93 percent of Clayton’s mobile-home loans had such costly terms that they required extra disclosure under federal rules. For the rest of the mobile-home lending industry, less than half of loans met that threshold. We also built this graphic to show just how different Clayton’s rates are to their peers -- MB

{kind=link}

what_comes_after_q29 karma

That is a comparison to regular home loan rates. Like you said in another post, these are not typical home buyers, and tend to have more credit risk. Seems like an extremely misleading comparison. If you want to compare them to an average, compare them to other mobile home lenders.

MobileHomeTrap-3 karma

I should clarify then: The comparisons I'm talking about are only for mobile-home loans. 93% of Clayton's mobile-home loans require extra disclosure. Less than half of everyone else's mobile-home loans require extra disclosure. The graphic is also dealing with just mobile-home loans. We aren't doing any comparisons to conventional home loans (the numbers there are much smaller). -- MB

CatsMakeGoodSnacks27 karma

How much at fault are the buyers of said homes for not being informed? Everyone knows trailer houses are notorious for depreciation, why would a person sign a poorly termed loan on something that doesn't hold value?

MobileHomeTrap7 karma

There is an information asymmetry between the borrowers, many of whom are financially unsophisticated, and the dealers, whose compensation depends in part on their ability to sell homes. If borrowers are treated fairly -- meaning they fully understand what they’re signing up for -- they certainly are responsible to repay any loan they agree to take out. However, we saw numerous cases where borrowers did not receive enough information to make an informed choice. Sometimes, they did not learn the terms of their loans until after making a deposit or spending money to prepare their land. Sometimes the loan terms changed after a verbal agreement. Some were promised the ability to refinance, even though Clayton’s lenders virtually never refinance mobile home loans.

The point is not to absolve borrowers of any responsibility for their decisions, but rather to highlight cases where those decisions were made with incomplete or misleading information that might have changed a borrower’s mind. -DW

Fixshit14 karma

"Sometimes, they did not learn the term of their loans until after making a deposit or spending money to prepare their land"

So the lender is at fault because some people are too stupid/lazy to do some research and figure out what they're getting themselves into? Or because they signed contracts without reading them?

MobileHomeTrap4 karma

Some of the customers we talked to are very intelligent and cautious people who say they were directly misled by company officials. As Dan mentioned, some borrowers said they didn’t learn the actual terms until making a deposit or spending money to prepare land. Some said they were pressured to take high monthly payments because they were promised a chance to refinance at lower rates in the future. Some said they were told Clayton financing was the only option.

Some of these folks really felt like they were doing due diligence. --MB

BunchOAtoms21 karma

How did you vet the people you talked to? These people seemed to have really bad credit (I didn't know it was even possible to have a credit score <500.), and I'm wondering how many of them were likely to be delinquent regardless. Did any of them just never pay their loan or make few attempts? I am usually skeptical of anecdotal accounts since every large company is, by the sheer nature of its size, going to have some bad actors that don't reflect the larger experience, and I was curious if this might be the case.

I read your rebuttle to the Clayton Homes statement, and I've got to admit that I felt like you were trying to use flimsy, conjectural stats to combat their flimsy, conjectural stats, and that didn't sit well with me. If you're going after them based on hard proof, then that's fine, but I felt like a lot of the story and the rebuttal was built on limited anecdotal evidence, as well as a lot of stats that were extrapolated out according to broad data not specific to Clayton Homes, but the industry at large. How would you respond to those concerns? I think the timing of this article and the Rolling Stone review is going to draw extra scrutiny to investigative pieces. Sorry to be that way, but I'm just a product of the current environment.

Lastly, as I understand it, manufactured housing is the only option for a lot of people who live in low-income rural areas who can't afford to purchase a house and also have limited, or non-existent, rental options. Is that correct? If so, what would be your solution to come up with housing for people who are a high credit risk with low incomes and have fewer options, if it's not Clayton Homes? In other words: "okay, so Clayton Homes is making high-cost loans; what is the alternative that's better?"

MobileHomeTrap9 karma

We examined loan documents and other documentary evidence underlying every anecdote that appeared in the story -- and dozens more related to stories that we didn’t have space to include. I personally did not encounter anyone who “never paid” or “made few attempts.” The people I talked to all sincerely thought they would eventually own their home and that it was a good investment.

We also took care not to rely exclusively on anecdotes. We relied heavily on Mike Baker’s analysis of federal loan data, which showed that most of Clayton’s loans qualify as “higher-priced” by government standards and among those, Clayton’s average 7 percent higher than prime loans, compared with 3.8 percent, on average, for other mobile-home lenders. These data are not about the industry at large; they’re about Clayton’s two lenders.

Regarding Clayton’s response, the company did not identify any inaccuracies in our report, or even present facts that mitigated our findings. Our response was an effort to add context and explain why Clayton’s response might mislead some readers. We would have loved to address some concrete data from Clayton about its lending rates, practices and loan performance, but the company ignored our requests for months.

It’s absolutely right that poor people in rural areas have limited options, and that they’re likely to pay higher interest rates than those with stronger credit histories. But some of the practices that numerous borrowers reported -- bait-and-switch, having thousands in fees financed into their loans, promises that they would be able to refinance -- are not a necessary byproduct of lending to a higher-risk population.

It’s worth noting that every year through the housing crisis Clayton Homes remained profitable.

Some advocates and regulators including the federal Consumer Financial Protection Bureau are looking at ways to better protect buyers of mobile homes. -DW

MobileHomeTrap7 karma

These are really good questions. We used hard numbers whenever it was possible: many numbers compiled from years of SEC filings; analyzing federal loan data to show things like market share on the national, state and local level; analyzing data to show how Clayton loans are particularly costly compared to peers; proprietary data provided from an industry consultant to describe loan failure rates; and data that the company describes in correspondence with regulators or in court filings.

That said, in some other aspects, you have to describe an array of anecdotes. There’s no data in the world that says “X% of all Clayton borrowers were promised refinancing.” But we heard that story repeatedly from consumers. There’s no data that says precisely how many Clayton borrowers were told to cut back on grocery and medical payments,” but we heard borrowers say that repeatedly. In some cases it was eerie to hear a borrower to voluntarily describe their experiences and have it be nearly identical to stories we’d heard from other people in other states. --MB

dementedavenger9917 karma

Multiple questions:

1) What was the impetus for this story?

2) Did any of the current/former Clayton customers you spoke to pursue legal action, contact state regulators, etc.? If so, is there an ongoing action?

3) How do you respond to the suggestion that your sample size of Clayton customers and former employees wasn't large enough. One could argue that your sample is representative; one could also argue that your sample is made up of motivated outliers.

4) Have you been surprised and/or disappointed by the lack of follow-on coverage by other media outlets (WSJ, CNBC, etc.)?

Edit: Grammatical error.

MobileHomeTrap10 karma

1) There are some other aspects of manufactured housing that really got me interested in the topic at first (Stay tuned. We expect more stories to come). For me, one of the biggest propellers on this story came when I really got a chance to analyze the federal HMDA data. The numbers were so surprising that I kept thinking I was messing up the data analysis. Could this company really be doing 39% of the new loans in the data? 6 times more loans than the next lender (Wells Fargo)? How can 93% of their loans be considered higher-priced? I figured I was doing something wrong. Turns out, I wasn’t doing anything wrong.

2) Some did contact state regulators to file a complaint.

3) We looked at over 100 loan files from 41 states. But our analysis of HMDA data looked at individual loan details on hundreds of thousands of loans. That really provided the context that Clayton differed from the rest of the industry.

4) I guess I don’t really have any expectations for that sort of thing. The story has been prominently featured on Business Insider, Huffington Post and other places. It’s a complex topic, so maybe others will pick up on it as time goes on. -MB

MobileHomeTrap6 karma

- I have been looking at predatory lending in the mortgage industry since 2006, before the financial crisis, so I stay in touch with housing advocates and consumer lawyers. More than one suggested I took a look at Clayton because their clients had experienced aggressive collections, collectors telling them to cut back on groceries or go on food stamps etc.

- Many of the borrowers are in Chapter 13 bankruptcy, hoping to save their homes by reducing the debt to somewhere around the value of the house. Many people have lodged complaints with state regulators and attorneys general. And there may be preliminary investigations -- for example, in Tennessee last year, frequent complaints about Clayton’s aggressive collection practices led state officials to contact local housing counselors seeking information about their experiences with the company, according to two people we talked to.

- We selected the vast majority of loan files from publicly available court documents, not just folks with axes to grind. But fundamentally when reporting on consumer abuse, it’s the people who are having problems that you need to worry about. This goes not just for Clayton but for any company that appears to engaged in such troubling practices.

- Not totally surprised that it would take the financial media some time to pick up the story. But it’s too early to say what kind of traction this will gain, especially with Berkshire Hathaway’s shareholder weekend coming up in early May. -DW

calreinvest17 karma

Do you see any similarities between Buffet making $ off of Clayton Homes and Buffet also making $ off of his sizable investment in Wells Fargo, whose foreclosure practices have been widely criticized?

MobileHomeTrap14 karma

Buffett has been a major investor in many financial businesses. He injected billions into Goldman Sachs and Bank of America during the 2008 financial crisis. He’s been a long-time shareholder of Wells. So clearly he thinks these are good investments.

Clayton is a different animal because it’s a vertically integrated company, combining manufacturing, sales, insurance and finance. Wells Fargo certainly isn’t building and selling houses -DW

MobileHomeTrap10 karma

Fun facts on this: Berkshire’s Clayton Homes did 39% of the industry’s new mobile-home loans in 2013. The second-biggest lender? Wells Fargo. -- MB

HyFikz11 karma

These customers do have a choice and if their credit and income is so bad that they need to take this route, it is fairly obvious they are going to be hit with a high interest rate

It is my understanding that they know all of this before purchasing one of these homes. At what point does it become the owners fault and not the purchaser? It is a business, not a government funded non-profit home supplier for the low income. Correct me if I am wrong, but I am not sure what your intended results are from this report?

All I see is a company that makes money, and charges a high interest rate to combat the high risk associated with the borrower defaulting on the loan. When people over extend themselves they get trapped all the time, it's easy to point the finger at someone else, but I think we all know who's fault it is.

MobileHomeTrap5 karma

Dan provided an answer here that answers this a bit, but I'll expand on it some more:

I know some of the borrowers that we spoke to really regret the trust they placed in Clayton’s representatives. The Ackleys spent $11,000 preparing their land after being told specific loan terms, then they said the terms changed dramatically at the closing table. Is it their fault for trusting the company? Several borrowers were pressured to take large payments because the company said they could later refinance to a lower rate. Is it their fault for trusting the company? Some buyers were told Clayton financing was the only option and didn’t see if they could get lower rates elsewhere. Is it their fault for trusting the company? Some of these folks thought they were being very cautious about the whole thing and ended up financially devastated.

There are also some unique aspects to this buying process, too. In a conventional home purchase, real-estate agents have a duty to represent the interests of the parties involved. A lender would generally work with an appraiser to make sure the home wasn’t overpriced or damaged in unseen ways. A closing attorney would manage the end of the transaction to make sure there are no misunderstood documents or sudden surprises. Those checks and balances often don’t exist in mobile-home transactions, so you end up with vulnerable buyers facing a high-pressure sales environment in which the manufacturer, retailer, lender and insurance broker may all be part of the same company. --MB

asmartguylikeyou11 karma

I have two questions. The first is what specific steps would you like to see Berkshire Hathaway take to rectify the "abuses" you have uncovered? I see a lot of "Look at what is going on here!!!" but not a lot of talk about potential solutions.

The second part of my question is actually to that point as well; to what extent do you believe there to are feasible solutions to some of the issues presented in your piece?

I see a lot of hand wringing over vertical integration along with a great deal of concern over the plight of Clayton's customers. I feel it is necessary to point out that a lot of these wrongs as you perceive them are the result of much larger structural issues that create the realities of rural poverty. You have high risk customers with terrible credit or with little to no credit history. There aren't a lot of lenders willing to service this customer base. Outside of a rural environment there would be other options for housing such as renting an apartment, or potentially federally subsidized housing, but when you live in the middle of nowhere you don't exactly have a lot of options.

A hundred years ago these folks would have built their own homes, and worked their own land. The collapse of the agrarian economy has left these communities not only underserved by potential lenders, but basically invisible to the wider culture. I have been to the places where a lot of these folks live. They are food deserts. They don't have access to basic government or health services. There are few opportunities for employment, and a lot of people subsist off of social security benefits. In this context someone without a place to live doesn't have a lot of options. One thing they often do have is land. Land to put a home on.

A local dealer selling you a manufactured home financed through one of the two major lenders is basically your only option. Now it is easy to point the finger and say "EXACTLY".-that these people are being taken advantage of, but when you are the only lender willing or capable of taking the risks, what exactly should you do? Stop providing your services altogether? If you are a potential customer who needs a roof over your head, what would you rather do? Go homeless, or pay more in interest because you can't qualify for a traditional loan. As for the idea that these homes should appreciate in value, that kind of goes against the whole point of the product. Mobile homes are cheap. They are cheap for a reason, because if they were expensive the people who need them wouldn't be able to afford them. Name one type item that you would purchase through a personal property loan that appreciates in value over time. I can't think of one.

I think it is easy to look at this and see nothing but predation and greed. I think the issue is much more complex than that. As I said earlier, these people are invisible. The issue of rural poverty is a non-issue in this country. The government has failed them. I appreciate the idea of giving these people a voice, but I think they need someone to advocate for them outside of the context of take-down piece of Warren Buffet. I mean it makes for compelling journalism "Billionaire Tycoon Builds Empire on the Back of the Everyman" but in reality the issues faced by these people are much deeper than the lenders that provide them with housing. It is my hope that that is the conversation that can come out of this.

Anyway, there is my rant. What would you like to see done, and to what extent do you believe the issues that you bring up are much more of a symptom, rather than the disease itself, of the wider structural issue of inequality and poverty in this country?

MobileHomeTrap2 karma

Thanks for the comment. You asked a good question about what steps could be taken to rectify problems here.

We focused in this story on the facts: Customer experiences, company policies, whatever data about loans and financial performance we could get our hands on -- and above all to portray those things accurately.

There are experts -- in the industry and outside the industry -- who have worked their whole careers on these subjects and who are better positioned to advance and debate policy proposals.

One thing that’s worth noting: 15 years ago, Congress asked HUD to examine ways to make mobile homes more affordable. HUD still hasn’t done the work.

-MB/DW

MobileHomeTrap13 karma

As Mike said, it can be cheaper than rent in some cases. But the cost of financing can offset the affordability of buying a mobile home. Buffett himself addressed that topic in his 2010 letter to shareholders (covering the 2009 calendar year): “For the all-cash buyer, Clayton’s homes offer terrific value. If the buyer needs mortgage financing, however – and, of course, most buyers do – the difference in financing costs too often negates the attractive price of a factory-built home.” -DW

MobileHomeTrap9 karma

It can be cheaper than rent. But the costly financing rates, long loan terms and dilapidating homes can also make it far more expensive than rent. Some buyers think they are buying a permanent asset to build equity, but we found that the depreciation of the homes can leave them underwater for years (See interactive here) One note: In our story, the Ackleys had monthly payments over $1,100 (after they described loan terms changing at the closing table). They lived in a very rural part of Washington state. You could potentially buy a decent conventional home for that size of payment. --MB

MobileHomeTrap3 karma

In the Ackleys' case, they said they had been told their monthly payments on their home would be $700 a month. Then they spent $11,000 at the urging of the dealer to build a concrete foundation to accommodate a specific home. After they finished all the work, they went to closing and were told the terms had changed and the new loan payment. They considered backing out, but they had already spent so much money up front. Plus, they said the broker told them they could refinance later. --MB

Kazomee9 karma

All of this is hearsay, which isn't to say that it's useless, but shouldn't there be some follow up. Maybe there was. Did you try to recreate the situation by acting as a potential buyer?

MobileHomeTrap0 karma

We really wish the company officials would have made themselves available to us. We asked numerous times to discuss our findings with both Clayton and Berkshire Hathaway. Unfortunately, the company ignored or declined our requests. We would still like to speak with them.

The mystery shopper idea is a bit tough. We never want to misrepresent ourselves. --MB

JPBLIII8 karma

Do you think that you might be painting the company with a very broad brush?

I have a Clayton Home that I am very happy with. Although my interest rate is higher than a conventional mortgage (personal property loan), I am paying $100 less per month for a 3 bedroom 2 bathroom home than I was in rent for a smaller 2/1 apartment.

MobileHomeTrap1 karma

We’re glad you’ve had a positive experience with the company, and we hope that continues. That has not been the case for many consumers who we spoke to. Our story was describing the challenges they have faced and whether the company’s practices have been consistent with Buffett’s public statements. -MB

ButtPuppett6 karma

While Buffett has a reputation as a responsible businessman and grandfatherly figure, we found that his company relies on predatory sales practices, exorbitant fees, and interest rates that can exceed 15 percent, trapping many buyers in loans they can’t afford and in homes that are almost impossible to sell or refinance.

If the 15% the average or are they specific, cherry picked examples from people with very low credit scores and high risk individuals?

MobileHomeTrap7 karma

The 15% is among the higher loan rates, but one document we have from the company says their typical loan rates range from 6.99% to 18%. The average of those we looked at was above 10%. I’d also refer you back to this chart, which shows that many of Clayton’s loans average about 7 percentage points ABOVE a typical home loan. -- MB

calreinvest5 karma

Do you think investors in Berkshire Hathaway are aware that they're making $ this way, and do you think they'll put any pressure on Buffet to stop these practices?

MobileHomeTrap3 karma

We’ve heard from a number of Berkshire investors who were shocked to learn of some of the practices detailed in our reporting -- so obviously many investors were unaware. And it’s incredibly difficult to learn details about Clayton from reading Berkshire’s public disclosures, so many would have no way to know what’s going on with this company.

It will be interesting to see if the issue comes up at Berkshire's annual shareholder meeting in Omaha -- what Buffett calls "Woodstock for Capitalists" -- in early May. -DW

strateego5 karma

Mike, you write that dealers use "tactics including last-minute changes to loan terms and unexplained fees that inflate loan balances."

Are their any safe guards to prevent last minutes changes to loan terms, especially after customers have prepared their property?

MobileHomeTrap8 karma

Not trying to dodge the question, but it’s important to say that we’re not lawyers and don’t draw legal conclusions. Some lawyers will tell you that these practices can violate state consumer-protection laws, but it depends heavily on the specific facts of the case. What we can say is: It’s unusual to disclose loan terms after money has been invested in the deal, and this appears to increase the potential for consumer abuse. -MB

MobileHomeTrap6 karma

We were looking at just one of his companies, not at his entire portfolio and certainly not at who he is. We don’t draw value judgments. -DW

ctmurray4 karma

How long did it take you to gather the information and write the article? And thanks for looking into this, such investigations by the fourth estate seem to be getting rarer.

MobileHomeTrap2 karma

Thanks for your kind words. I have been working on the topic exclusively since last October. We were fortunate to join forces with Mike and The Seattle Times, who already were looking into these issues, in early February. -DW

MobileHomeTrap2 karma

Thanks! I have heard about issues in this mobile-home industry for a long time but really started focusing on the topic when I was finishing a different project last year. Hopefully we'll have more to come. --MB

Xanola3 karma

Sorry if this is in the article and I missed it, but do you have a list of all of the companies that Berkshire Hathaway does business as or owns?

MobileHomeTrap3 karma

Here’s a link to Berkshire’s site and their listed companies: http://www.berkshirehathaway.com/subs/sublinks.html

It’s worth noting that many of those companies can have many subsidiaries that aren’t listed. Clayton, for example, has a list of its various home brands on its website And its dealers go by many names -- Clayton, Oakwood, True Value, Luv Homes, Freedom, SouthernHomes. The company refused to provide us with a comprehensive list.

Clayton’s lenders go by the names of Vanderbilt Mortgage and 21st Mortgage. Its insurance broker is called HomeFirst Agency. -DW

Chip892 karma

You Guys Know Ford also does there own Loans though Ford Credit? But you know there not a scam!

MobileHomeTrap5 karma

Lots of companies have captive finance arms, and some may be worthy of investigation. For this project we were looking specifically at Clayton, which is by far the biggest builder and lender in the mobile home business. One fact particular to Clayton is that it has two lenders and numerous brand names for its retailers. Lots of customers we talked to didn’t realize before they signed that the lender and the dealer were the same company. -DW

CurtNo-1 karma

Do top comments need to be in the form of a question? And have a question mark?

CurtNo2 karma

Read most of it, thanks. Also told my coworker about it. He's a huge Buffet fan, gave us Buffetology books for Christmas. Needles to say he wasn't too thrilled, a good example of cognizant dissonance.

I'm tired of the term "predatory loans" being overused. A contract (mortgage) is between two people. If one of the two is foolish, the other is not necessarily a predator.

So, while I have empathy towards the supposed "victim," its not like they weren't complacent.

The real problem is the false economy driven by centrally planned interest rate. Currency is cheap, and the risk of bank loss to defaulting borrowers is insured by current tax payer, and future generations. Intentional Moral hazards all around.

So, while you target Buffet (a righteous goal) you miss the underlying problem... central planning by a central bank. Get rid of the false interest rate, bring back risk, and predatory Buffets will cease to exist.

MobileHomeTrap8 karma

Interesting fact: Some 20 million Americans live in mobile homes. -MB

gbimmer-6 karma

I have no idea why so many respect him.

Did you happen to find out more about him supporting the increased estate taxes so the inheritors would have to sell their inheritance for cheap to pay taxes? Does this apply to the mobile home business?

iia76 karma

Wouldn't high interest rates make sense when dealing with a demographic who are more likely to default on their payments than those who make a higher income?

Also, don't the contracts explicitly detail the rate changes?

View HistoryShare Link