MobileHomeTrap

Highest Rated Comments

MobileHomeTrap13 karma

As Mike said, it can be cheaper than rent in some cases. But the cost of financing can offset the affordability of buying a mobile home. Buffett himself addressed that topic in his 2010 letter to shareholders (covering the 2009 calendar year): “For the all-cash buyer, Clayton’s homes offer terrific value. If the buyer needs mortgage financing, however – and, of course, most buyers do – the difference in financing costs too often negates the attractive price of a factory-built home.” -DW

MobileHomeTrap12 karma

As a whole, mobile homes are financed at higher rates than conventional homes for a couple of reasons: First, because many of them are personal property loans like you’d get on a car, as opposed to mortgages. Second, because conventional loans benefit from various forms of government support.

It’s important to keep in mind, though, that the subprime lending business on homes has essentially been defunct since the 2008 crash. -DW

MobileHomeTrap11 karma

Regarding the first part of your question, credit risk always is a part of how loans are priced. However, Clayton’s loans are unusually costly, as Mike explained in this answer, in part because Berkshire Hathaway charges Clayton up to an extra percentage point on top of BRK’s own borrowing costs -- and that’s passed directly to the consumer. So credit risk is only one element of how the rates are set.

On your second question: Many borrowers said they were induced by Clayton sales reps to spend money preparing land or paying deposits before they found out the loan terms. These people don’t have much to spare, so they can feel trapped by the money they already have invested. -DW

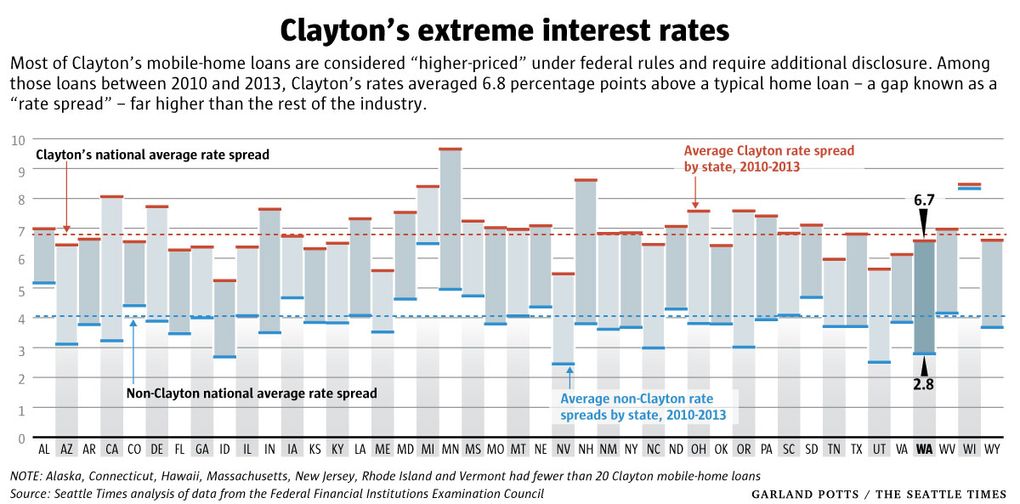

MobileHomeTrap11 karma

If you just look at mobile-home lenders, Clayton has some particularly costly rates. During the most recent four-year period, 93 percent of Clayton’s mobile-home loans had such costly terms that they required extra disclosure under federal rules. For the rest of the mobile-home lending industry, less than half of loans met that threshold. We also built this graphic to show just how different Clayton’s rates are to their peers -- MB

{kind=link}

MobileHomeTrap14 karma

Buffett has been a major investor in many financial businesses. He injected billions into Goldman Sachs and Bank of America during the 2008 financial crisis. He’s been a long-time shareholder of Wells. So clearly he thinks these are good investments.

Clayton is a different animal because it’s a vertically integrated company, combining manufacturing, sales, insurance and finance. Wells Fargo certainly isn’t building and selling houses -DW

View HistoryShare Link